Good Morning!

I am pleased to announce that the new site is up and running. From now on, all posts can be found at http://www.futurescommentary.com/

You will find improved functionality, including the ability to subscribe by email!

I hope you enjoy the new site, and I look forward to hearing your feedback.

Best regards,

Jaime Macrae

Tuesday, May 24, 2011

Friday, May 20, 2011

Price Dictates Priorities: Crude Oil Rig Count Surpasses That for Natural Gas - May 20th

Price Dictates Priorities: Crude Oil Rig Count Surpasses That for Natural Gas

May 20th, 2011

Energy producers in the United States United States

U.S. Crude Rig Count vs. Crude Oil

Courtesy of Bloomberg

U.S. Natural Gas Rig Count vs. Nat Gas

Courtesy of Bloomberg

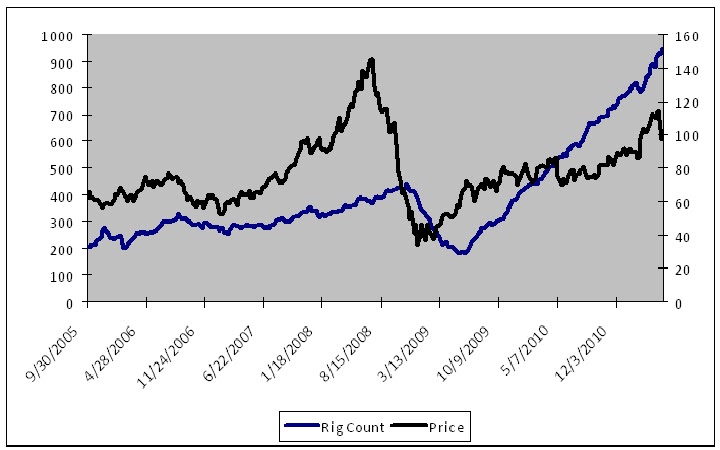

The natural gas chart shows that as the price of natural gas fallen over the past three years and found stability in the $4 - $5 range, drilling activity has declined as well. Conversely, the number of rigs drilling for oil has risen rapidly as prices have rallied over the same time period. What makes this particularly interesting this morning is the for the fist time since the early 1990s, more rigs are now drilling for oil than are drilling for natural gas (see chart).

U.S. Rig Count – Nat Gas vs. Crude Oil

Courtesy of Bloomberg

At first glance this would seem to portray a natural gas market that is setting the stage for another major rally, but it is important to realize that with improved drilling techniques producers are yielding more gas from each well, and production has actually increased 7 percent since 2008 when the rig count began to fall.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Thursday, May 19, 2011

Drought or Flooding: Mother Nature is determined to disrupt the Wheat Crop - May 19th

Drought or Flooding: Mother Nature is determined to disrupt the Wheat Crop

May 19th, 2011

One way or another, wheat crops around the world are suffering from adverse weather conditions. Some areas are struggling to get the crop planted amidst major flooding, while others are seeing their crop whither in extreme drought. While global stockpiles are substantial, and there does not seem to be any prospect of a serious shortage, this year’s crop seems doomed to disappoint.

Spring Wheat Planting

Farmers in the Dakotas are having a very difficult time planting this year’s crop of spring wheat (the variety traded in Chicago

Winter Wheat in the Southern U.S.

Farmers in the South, specifically in Texas and Oklahoma Kansas City

International Droughts

To the east, there are similar conditions being reported in

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Wednesday, May 18, 2011

Structurally Bullish Palladium

Structurally Bullish Palladium

May 18th, 2011

The fundamental backdrop for palladium continues to improve, moving from a surplus of 680,000 ounces a couple of years ago to a shortage of 490,000 ounces last year. Johnson Matthey Plc, one of the top dealers and analysts in the PGM space, is forecasting the largest supply deficit in a decade in 2011.

Demand

The biggest source of demand for palladium comes from automobile producers, who use the metal in catalytic converters. While demand from this space fell dramatically following the financial crisis and ensuing economic contraction, it has since rebounded and is now at a record high. Consumption from car manufacturers jumped 35 percent last year to 5.45 million ounces.

Another big source of demand, which is relatively new, is from investors buying physically backed ETFs, much like the well known GLD or SLV. These funds have only been buying the metal for a few years, and have accumulated 2.173 million ounces so far. Last year they bought 1.09 million ounces, up 74 percent from a year earlier. As more and more retail investors turn to commodities, and specifically metals, as a store of value and a hedge against what seems to be inevitable inflation, this could prove to be a significant source of future demand.

All told, total demand rose 23 percent last year to 9.63 million ounces.

Supply

The supply of palladium is a little bid weird. The largest source comes from South African mines, which traditionally produce between 2.5 to 3 million ounces. The second biggest source are the Russian mines, however Russian production is supplemented by sales from government stockpiles. The government sales, which last year totaled 1 million ounces, are seen as crucial to maintaining balance to this market which would otherwise be in perpetual and very serious deficit. The catch is that the quantity of government stockpiles is a closely guarded state secret, so it is impossible to predict if and when these sales will dry up. Standard Bank Group Ltd. has predicted that they will be depleted as early as this year, though it is unclear what this prediction is based on.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Tuesday, May 17, 2011

Weakness in the Cocoa Market - May 17th

Weakness in the Cocoa Market

May 17th, 2011

The cocoa market continues to come under pressure, with a string of bearish developments in West Africa . There are several main points that are weighing on the market.

1 – The four month political standoff that had turned violent, and caused the cocoa trade to grind to a halt, is now over.

2 – The export ban has been lifted in the Ivory Coast

3 – The banking sector has resumed operation in Abidjan

4 – Major commodity firms have returned to the Ivory Coast

5 – Large stockpiles that had built up in warehouses in Abidjan

6 – Production is forecast to have grown significantly from last year, up 100,000 tonnes in the Ivory Coast

7 – Output in Guana has boomed, with forecasts for a crop of 920,000 tonnes, up from 632,000 tonnes last year. It is commonly believed that smuggled cocoa from the Ivory Coast

The bull camp points out that there is currently around 500,000 tonnes of cocoa stored in warehouses in the Ivory Coast

All told, the outlook for the price of cocoa is not good.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Monday, May 16, 2011

Speculators Shun Copper - May 16th

Speculators Shun Copper

May 16th, 2011

Last month I wrote about the copper market, noting that it looked top heavy and I examined some changes taking place in China

CFTC Large Non-Commercial Traders vs. Price

Courtesy of Bloomberg

The speculative community has held a large net long position since last summer, and over the past few weeks have been liquidating their positions en masse. Open interest has been declining steadily as well, indicating reduced speculative participation in the market. While there are many factors in determining the market price of copper, this is yet another strike against the red metal.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Friday, May 13, 2011

Canadian Dollar - May 12th

Canadian Dollar

May 12th, 2011

The loonie has drifted lower over the past couple of weeks; this morning trading down to the low end of the channel in which it has been appreciating steadily since last year. Despite the weakness in absolute terms, the Canadian dollar has shown impressive strength over the past week when viewed against a backdrop of rapidly declining commodity prices. Crude oil and the Canadian dollar have a very strong positive correlation, as the fossil fuel is our nation’s largest export, so in the face of a double digit decline in the price of oil it is reassuring to see the currency continue to trend higher. The same is true with regards to the price of gold.

Below is a weekly chart of Canadian dollar futures over the past year. As you can see, the appreciation has been steady and unwavering. When compared to the dramatic rise in other similar currencies, specifically the Australian and New Zealand

Canadian Dollar Futures - Weekly

Courtesy of Bloomberg

The Fundamentals

One of the most important determinants of a currency’s trend is the differential between the interest rates in the two countries. When the interest rate is higher in one country, that nation’s currency tends to strengthen relative to the other. The reason is easy to understand. To illustrate, let’s look back in time to the once ubiquitous ‘yen carry trade’.

Monetary policy in Japan has been extremely accommodative for many years, as the central bank embraced a policy of zero interest rates in an effort to stem persistent deflation, as policy know as ZRIP (zero interest rate policy). Meanwhile, further south in Australia Japan

The Bank of Canada followed the Federal Reserve’s lead and brought the overnight lending rate down to a record low of 25 bps in April of 2009; the Fed had reduced their rate to a band between 0 and 25 bps a few months earlier in response to the financial crisis. By mid 2010 however, the Canadian economy was recovering well, and inflationary pressure pushed the BOC to start raising rates, which they have now done three times, bringing the overnight rate to 1 percent. The Fed is unlikely to raise rates anytime soon, so this is a long term positive for the Canadian dollar that could persist for years into the future.

The Federal Reserve had embarked on a path of money creation on a scale that is unprecedented. Despite rhetoric about the ‘benefits of a strong dollar’, it seems evident to most that there is a concerted effort to devalue the U.S. dollar in order to boost export markets, and inflate their way out of an unsustainable debt situation. Canada

All told, the outlook for the Canadian dollar is very positive.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Wednesday, May 11, 2011

USDA Supply and Demand – Corn and Soybeans - May 11th

USDA Supply and Demand – Corn and Soybeans

May 11th, 2011

This morning the USDA released its first supply and demand estimate for the 2011/12 crop year, as well as an update on last month’s report for the marketing year. Below are the highlights:

Corn

The immediately bearish headline was the increase in the projected ending stocks for the current marketing year, up to 730 million bushels from 675 million bushels last month. This probably reflects declining export demand in the face of record high prices. The past several weeks have seen sharply lower exports, below the level required to meet USDA expectations. This is necessary, as without some rationing the U.S.

The first estimate of ending stocks next year was 900 million bushels, still very tight by historical standards, and while it is likely to be construed bearishly in the short term, could provide long term support for new crop prices.

Drilling a little bit deeper into the USDA’s numbers, it is interesting to note the estimate for ethanol demand, which has slowed to almost no growth. After rising 23.2 percent in 2010, and 9.5 percent this year, the USDA projects demand for ethanol to rise a paltry 1 percent in 2011/12. Projected demand for the alternative fuel is probably the most important determinant of price of corn after production, as more than 40 percent of the crop now goes towards ethanol. Until recently, blenders were allowed to add up to 10 percent ethanol into their gasoline, earning a nice tax credit, not to mention reduced costs as ethanol prices still lag those for the fossil fuel. At the current level of production, ethanol is pushing up against that 10 percent ceiling as compared to gasoline production. Recently, regulation was approved to allow up to 15 percent ethanol in gasoline blends for newer vehicles. If the ethanol industry increases production to take advantage of the higher blend rate, the USDA’s estimate could prove to be too low, pointing to tighter than expected ending stocks.

Soybeans

USDA projected ending stocks for soybeans were also revised slightly higher, up to 170 million bushels from 140 million last month. Once again, this is probably due to declining exports. China has released beans from its official reserves in an attempt to ease food price inflation, reducing demand for U.S.

The interesting bit from today’s report is the reduced export demand, down to 1.54 million bushels from 1.55 this year. Export demand is the key driver of soybean prices in the U.S. China is the largest importer of U.S. China U.S.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

Tuesday, May 10, 2011

Flooding on the Mississippi is putting a Bid under Gasoline Futures - May 10th

Flooding on the Mississippi is putting a Bid under Gasoline Futures

May 10th, 2011

With the exception of silver, gasoline has been the star commodity since last week’s broad commodity selloff, up 7.77 percent since last Thursday. It is worth noting, that over the same period, heating oil, which is a closely related distillate, has risen only 4.24 percent, and crude oil has rallied only 5.27 percent. Unlike the other energy products, gasoline is now trading near its recent peak. The question is why.

Seasonality plays a role. As I have discussed in recent posts, gasoline tends to get more expensive relative to its related products during the summer months, when people spend more time on the road. The summer driving season officially kicks off on Memorial Day later this month. While this is certainly a bullish factor, it does not on its own explain the strength in the gasoline market. What is more important at the moment is the risk of significant production losses stemming from flooding on the Mississippi River .

Grain traders are already well aware that the flooding along the U.S. ’s largest river system, which drains 41 percent of the continental U.S. Missouri Louisiana

There is now talk of opening the Morganza Floodway to relieve the flood threat between New Orleans and Baton Rouge U.S.

Monday, May 9, 2011

Inter-commodity and Calendar Spreads - May 9th

Inter-commodity and Calendar Spreads

May 9th, 2011

After any large shift in the market, such as last week’s extremely volatile session, I prefer to wait a few days before looking at any new trade ideas, in other words ‘wait for the dust to settle’. I will therefore use today to discuss spread trading in futures markets. There are two broad categories of spread trading: inter-commodity and intra-commodity (calendar) spreads.

Inter-commodity Spreads

An inter-commodity spread entails buying one commodity and selling another related commodity, expressing a view on the relationship between the two contracts irrespective of the overall direction of the market. This type of trading can be an excellent way of gaining exposure to a class of commodities (such as the energies, or grains), without a strong opinion on the outlook for the market in general. By inoculating the trade against the movements of the broad market, it is possible to profit in both upward trending and downward trending markets. Let’s look at some recent examples.

On March 29th, 2011 I wrote in this blog:

“The general rule of thumb when it comes to the seasonality of the refined products is that heating oil is strong in the winter months, when demand rises in response to cold weather, and gasoline is strong in the spring/summer months when more people ‘hit the road’ boosting demand for the fuel. This seasonality is clearly demonstrated in the forward curve for RBOB gasoline futures, with higher prices seen in the summer months.

Spread Between RBOB Gasoline and Heating Oil

Courtesy of Bloomberg

As the chart above demonstrates, (with the exception of 2008) gasoline generally trades at a premium to heating oil starting somewhere around February or March, and trades at a discount sometime towards the end of the summer. Currently the two products are trading at nearly the same price, and the trend is in favour of the RBOB, as would be expected based on historical seasonality.”

Since then, the spread has moved steadily in favour of the gasoline (see chart).

Spread Between RBOB Gasoline and Heating Oil

Courtesy of Bloomberg

What is even more important to note, however, is how that spread has behaved over the past few sessions. On Thursday of last week, the refined products fell precipitously, with June heating oil falling 2561 points, and June RBOB gasoline futures falling 2271 points. The spread moved 290 points in favour of gasoline. Since the plunge, markets have been recovering. This morning the heating oil is up 531 points and the gasoline is up 1088 points. Again the spread has moved in favour of the gasoline, by 507 points. This shows that when you are correct about the direction of the spread, you can profit even during the most tumultuous of markets.

Intra-commodity Spreads

The other common variety of spread trade is the intra-commodity or calendar spread, when you buy a commodity for delivery in one month, and sell the same commodity for delivery in another. This type of trade expresses an opinion on differences in supply and demand during different type periods. It is very commonly used in grain trading, especially when the months reflect different crop years. Last week I wrote about one such spread in the corn futures, specifically the spread between July and December futures, or old and new-crop corn.

I wrote, “In recent years, December futures have tended to trade at a 15-30 cent premium to July futures. This year however, due to extremely tight physical supply, old-crop July futures have been trading at a steep premium to the new-crop December futures. The spread peaked earlier this year at $1.33 ½ July over, and has since been declining. Given recent developments, namely the difficulties planting the corn crop and thus the possibility of a smaller crop, and the waning demand for old-crop corn, this spread could continue to narrow.”

At the close prior to that comment, the July futures were trading at a 73 ¼ cent premium to December. Corn did not sell off as violently as most markets last week, but declined nonetheless. This morning the corn market is trading higher. Since that comment was written however, the spread between July and December has narrowed to 47 ½ cents. By trading the spread and not taking an outright position in the corn, we were able to make money in both up and down markets.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Thursday, May 5, 2011

A Comment on the Psychological Nature of Trading - May 5th

A Comment on the Psychological Nature of Trading

Anyone sitting in front of a quote terminal this morning, is either jubilant (hopefully because they’ve been reading this blog and have some short positions in copper, cocoa, and silver, not to mention a favourable calendar spread in corn futures – offset of course with a still-profitable long position in the coffee that is suffering from a big decline), or experiencing a serious drawdown. I will forego any specific discussion today, and focus instead on some of the psychological hurdles to successful trading.

Profits can be addictive, and at times seem to come easy. In my experience, early success in trading can be one of the worst things to happen to a new trader, as it builds unrealistic expectations for future profits, which can often lead to overly aggressive trading when times are tougher, often resulting in losses. On a day such as today, when the absolute size of the moves whether they are up or down are very large, quick mental calculations will taunt even the best of us… “Short just one silver contract would give me a profit of $16,500 today alone!”

Whenever I find myself entertaining notions of trading in such a market, I take a cold shower and remember what my top priority must be: MANAGING MY RISK. Quick and easy profits are certainly attractive, but ‘quick and easy’ is misleading, and incredible profits can quickly turn into devastating losses. My advice: Take a deep breath and remember why you entered into your various positions. What has changed? Take a step back and think about what your exposure is. Is it time to take something off the table, reduce your risk, or place some stops? Whether you are on the right side of the big moves or not, volatile markets call for defensive trading. Keep your head and you’ll keep your capital as well.

Good luck and happy trading!

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Wednesday, May 4, 2011

Normalcy Returns to the Cocoa Market

Normalcy Returns to the Cocoa Market

May 4th, 2011

One of the last remaining barriers to normal trade out of the Ivory Coast

A return to normalcy may put pressure on cocoa prices, which are still 65 percent above the 5-year average. The sharp increase in the price of cocoa was largely due to the stalled trade in the Ivory Coast

Farmers in the West African country have just begun to reap the mid-crop, the smaller of the two annual harvests, which typically puts seasonal pressure on prices. There is also more than 500,000 tonnes sitting in warehouses in the commercial capital of Abidjan Abidjan

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Tuesday, May 3, 2011

Corn Spreads - May 3rd

Corn Spreads

May 3rd, 2011

New Crop Corn

Farmers in the United States Nebraska is behind by 20 percent, Indiana by 29 percent, Illinois by 36 percent, Iowa by 40 percent, and Minnesota South Dakota Corn Belt , which could help farmers, and it is important to remember that with modern farm technology, the crop can be planted in an astonishingly short period of time. As usual for this time of year, Mother Nature is driving markets.

Old Crop Corn

The supply situation is extremely tight, as discussed in earlier posts, and in order to maintain sufficient stocks through the end of the crop year, demand must cool off. The record high price of old crop corn does seem to have brought about the rationing the market so desperately needs, and export sales have been slowing down. Weekly export inspections showed exports at 34.63 million bushels last week, down from 36.58 million the week earlier. This compared to the 44.09 million tonnes required each week to meet the USDA’s export projections for the year. Cumulatively, 59.3 percent of the USDA forecast has been exported, compared to 63 percent on average for this time of year.

Old-New Corn Spread

In recent years, December futures have tended to trade at a 15-30 cent premium to July futures. This year however, due to extremely tight physical supply, old-crop July futures have been trading at a steep premium to the new-crop December futures. The spread peaked earlier this year at $1.33 ½ July over, and has since been declining. Given recent developments, namely the difficulties planting the corn crop and thus the possibility of a smaller crop, and the waning demand for old-crop corn, this spread could continue to narrow.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Monday, May 2, 2011

A Catalyst for a Bull Market in Natural Gas? - May 2nd

A Catalyst for a Bull Market in Natural Gas?

May 2nd, 2011

Natural gas has been stuck in a protracted bear market after making a significant high in 2008. One of the biggest factors weighing on the price of natural gas is the continued expansion of shale-gas production in the United States U.S. U.S.

Nymex Natural Gas Futures

Courtesy of Bloomberg

It has been my view for some time that the proliferation of shale-gas development would keep a ceiling on natural gas prices in North America , with a few possible developments that could spark a sustainable rally. One of which would be significant investment in LNG export capacity, which would provide a link between domestic prices and the world market. Currently, the North American benchmark is around $4.50 versus around $8.00 in international markets. Another potential catalyst for a bull market in natural gas would be legislation that hampers the development of shale gas resources, possibly due to environmental or health concerns. Some recent developments in the U.S.

The FRAC Act

The Fracturing Responsibility and Awareness of Chemicals (FRAC) Act, introduced in June 2009, would require public disclosure of the chemicals used in the hydrofracking process. Hydraulic fracturing involves pumping heated and pressurized water, mixed with a cocktail of chemicals, into shale formations, separating the rock and allowing the gas to escape. Under current regulation, companies are exempted from disclosing which chemicals are used, arguing that they must maintain the secrecy of the ingredients for proprietary reasons. The Energy Policy Act of 2005 exempted the process from regulation by the EPA under the Safe Drinking Water Act, a rule commonly called the ‘Halliburton Loophole’. Since its introduction, the FRAC Act has been under review by the Subcommittee on Energy and Environment but never came up for debate. Under Congressional rules, any legislation that did not come up for debate is cleared from the books once the session ends. As a result, this Bill is no longer under consideration, though members often reintroduce bills once the new session begins. Recent developments seem to support the notion of this legislation making a comeback, though its ultimate fate is far from certain.

Diesel Fuel Discovered

The aforementioned ‘Halliburton Loophole’ does not exempt the process from regulation in cases where diesel fuel is used, due to the high level of toxicity and risk it poses to drinking water supplies. A year-long investigation that released its findings in January of this year found that between 2005 and 2009, at least 32.2 million gallons of diesel fuel was pumped into the ground as part of fracking operations in 19 states, in violation of the mutually binding agreement between the government and the energy companies. Diana DeGette, who first introduced the FRAC Act, and who is currently a ranking member of the Subcommittee on Oversight and Investigations said in a statement, “Our investigation has shown that for the past several years, the fracking industry has ignored federal regulations and a mutually binding agreement, and injected over 30 million gallons of one of the most toxic chemicals into the ground, potentially contaminating drinking water aquifers in communities nationwide,”. This could help open the door to further regulation.

Most Recent Findings

On April 18th, 2011, a report from the democratic members of the House Energy and Commerce Committee and House Natural Resources Committee revealed the use of 29 different chemicals regulated under the Safe Drinking Water Act as potential human carcinogens. The report highlights the potentially harmful effects of the hydrofracking process on human health, and could help build support for a re-emergence of the FRAC Act in the current congressional session.

Any move to tighten regulation of hydraulic fracturing may have a significant impact on future natural gas supplies, and could be the catalyst to mark the bottom in this protracted bear market.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Friday, April 29, 2011

U.S. Government Debt, the Decline of Fiat Currencies, Gold and the Fed - Apr 29th

April 29th, 2011

The USD against Other Currencies

The U.S. dollar has been falling precipitously against virtually every major currency around the world. Sentiment is reaching extremely low levels, and based on the CFTC’s Commitment of Traders report, speculators are short of the greenback in every major pair, with the exception of the Japanese yen. Below is a chart of the net USD position of large non-commercial traders (typically interpreted to represent the positions of large hedge funds and trading desks), overlaid against the U.S. Dollar Index.

U.S. Dollar Index and Net Large Speculative Positions

Courtesy of Bloomberg

During this week’s post FOMC press conference, the first of its kind, Fed Chairman Ben Bernanke was asked about the Fed’s stance on falling U.S. dollar. He was very clear that the Fed believes that a strong dollar is in the nation’s best interest. If he believed what he was saying, it seems no one else did, as the U.S. dollar proceeded to make new lows.

The U.S. Dollar against Non-Fiat Stores of Value

It is always important to remember that when we look at currency values, it is always relative to another currency, but how are fiat currencies doing in general when measured against some other tangible store of value. The obvious example are the precious metals, and more specifically gold. Gold has been rising steadily, making new all-time highs on 14 days in April. Some might argue that gold is not money, but tell that to Utah

Gold in USD and Aussie

Courtesy of Bloomberg

Inflation

If you were to listen to Bernanke, the only thing pushing inflation higher is the rising gasoline price at the pump, which is the result not of a weakening U.S. dollar and overly accommodative monetary policy, but outside geo-political events in the Middle East and North Africa . Let’s turn instead to reality. Over the past 12 months, virtually every commodity has seen significant gains, with few exceptions. The prices of raw material are highly sensitive to excess money creation, and are a fantastic leading indicator of current and future inflation. This is not “transitory” as some would like us to believe.

To the Point: U.S.

Given that the U.S. dollar is in decline, and inflation is on the rise, why are investors willing to lend money to the U.S.

-Jaime Macrae, CIM

Account Executive, Friedberg Mercantile Group

jmacrae@friedberg.ca

Subscribe to:

Posts (Atom)